Bill Haywood, a Steward at UE Local 814, was circulating petitions supporting the “Medicare for All” bill in Congress but ran into some problems. He approached Lois, the union president, “Lois, I need some more facts. Lots of people are complaining about how expensive our current health insurance is, but they have questions about what single payer health insurance is. Do you have something that will help members see how much money they will save under Medicare for All?”

What is Medicare for All single payer health insurance?

- Single-payer national health insurance is a system in which everyone can get the health care they need and doesn’t have to worry about how they will pay for it. A single public agency organizes health financing through taxes. Instead of numerous for-profit insurance companies handling payments, there would be one agency, like the Medicare administration, that would pay all the bills.

- No more money would be wasted on insurance company profits, high salaries of executives, advertising and marketing.

- No more time would be wasted seeking pre-approval from insurance for care your health care provider has deemed necessary.

- People would no longer face copays to receive care or prescriptions. People would have access to regular preventative check-ups and their full prescribed doses of medications, which would not only improve health but also bring down medical costs by preventing expensive care interventions that arise when people put off seeking treatment or can’t afford to take their medicines as instructed.

- The new, government-provided health insurer would be the only game in town for medical providers, and can use its collective bargaining power (a concept we are familiar with) to negotiate lower rates for procedures, prescription drugs, and medical devices.

- People would have the right to see the doctors and use the hospitals they choose. There would be no need to see which providers were “in network” because everyone would be.

- Care would be comprehensive, including preventative and emergency health care, as well as dental, vision, mental health, and long-term care.

How would your finances improve under Medicare for All?

One of the most common complaints of UE members is the rising cost of health care. This isn’t imaginary. Health care costs in the U.S. have risen much faster than inflation, and more of those costs are being passed on to workers.

Under Medicare for All, workers and employers would pay for health insurance through a payroll tax. However, this payroll tax would be far less than both workers and employers pay right now--and there are no copays later! While the exact payroll tax amount has not yet been settled, a common estimate is double the current Medicare tax (which is 1.45% for workers), so about 3% of income.

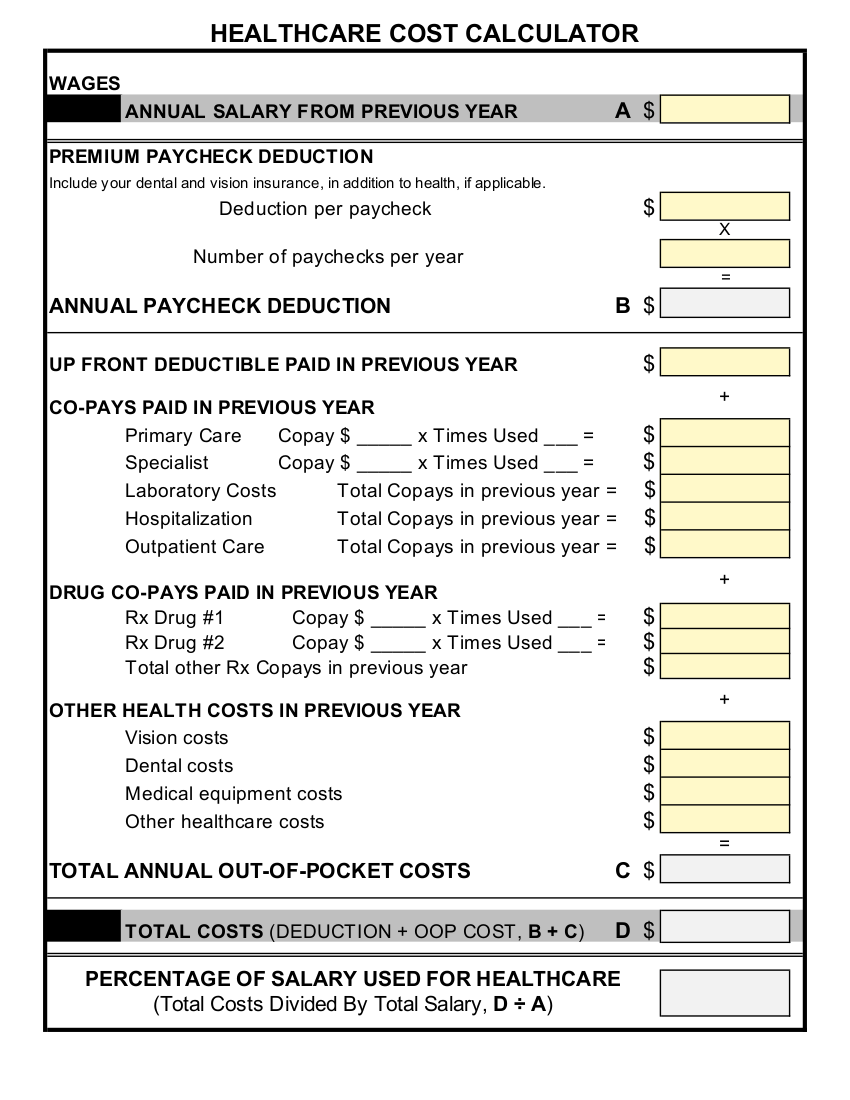

To understand how this would really impact you and your family, use our health care costs calculator to help figure that out. Starting with your current income and health care costs, like premiums and copays, see how much you currently spend on health care. If what you are paying is more than 3% of your salary, you’re likely to spend less money under a single payer program. So far, almost all UE members who have used it have found they will save money under Medicare for All. You can find an interactive online version at healthcosts.ueunion.org.

What would it be like to receive care?

It can be intimidating to think about changing from a familiar system to something that is different. Many workers in the United States don’t realize how much simpler it is to receive health care in countries with a single payer system. Moving to a Medicare for All system will remove many of the obstacles to receiving health care which we have to put up with now. Let’s look at what that would look like in practice for someone to see a doctor, nurse practitioner, therapist, or other health care provider.

| Current System | Medicare for All | |

|---|---|---|

| Payments | Pay for insurance premiums through your employer or health care exchange, plus deductibles and copays when you actually seek care. | Pay for insurance through payroll taxes. That’s it. |

| Care Decision | Decide you may need some medical, dental, or mental health care. Self-assess whether or not this care is urgent or can be delayed, depending in part on your ability to pay for fees associated with the needed care. | Decide you may need some medical, dental, or mental health care. Choose a health care provider that can assess your needs. |

| Emergency Care | If you have a medical emergency, decide if you will call 911 and pay surprise fees that sometimes arise from emergency medical services or ambulance transport. If not, figure out a different way to get to emergency care. | If you have a medical emergency, call 911. Emergency medical services and ambulance transport are covered. There won’t be surprise bills later. |

| Appointments | To get an appointment with a health care provider, first ask if they accept your insurance. Then proceed to book an appointment. Depending on options in your area, you may wait weeks or longer for care. | To get an appointment with a health care provider, call whomever you’d like to see and ask for an appointment. (Under Canada’s single-payer system, there are no delays for primary or urgent care.) |

| Rx and Follow-up | If your health care provider prescribes medication or follow-up care (such as physical therapy or seeing a specialist), spend time finding out if it is covered by your insurance. If it is covered, consider whether or not you can afford the associated copay. If it isn’t covered, consider whether or not you can afford to pay for it entirely out of pocket. | If your health care provider prescribes medication or follow-up care (such as physical therapy or seeing a specialist), fill the prescription or book the appointment for follow-up care. You won’t have any extra fees. |

| Bills | After completing your care, wait for a bill from the provider. It might just be your copay, or there might be additional fees. | There are no extra bills after care. |

Under Medicare for All, workers never worry about losing health care again if you:

- Change jobs

- Lose your job

- Decide to retire early

- Have a short- or long-term disability

- Are out on workers’ compensation

- Go out on strike!

For more information about Medicare for All or how to get involved in advancing this legislation, visit ueunion.org/medicareforall.

What is it like for workers to get health care under Canada’s single-payer system?

In January 2020, UE members met with members of the Canadian union Unifor over Zoom to talk about different experiences getting health care. When asked to describe what a general visit for health care is like, Katha Fortier, assistant to Unifor’s national president, said, “I have a great family doctor. If it’s urgent I can usually get in to see her the same day. Something like a physical, then you’d have to schedule that in advance. There’s no cost. You just go to your doctor and have your visit. If your doctor is on vacation or something, my doctor is part of a clinic, and there’s a variety of other doctors that can see you.”

Katha noted that she lives in Toronto, so she asked one of the members who lives in a more rural area to speak about their experience. Barb Maki is a member who works in health care and lives in rural northern Ontario. She said, “You can see somebody at a clinic. We don’t have a long wait time.”

Barb later shared her experience about needing emergency treatment for a broken ankle, for which she had to have surgery. She said, “There was no wait. I saw an orthopedic surgeon immediately in the emergency department, and they did the surgery first thing the next morning. There was no cost to me for any of this.”